2012 · Washington D.C., United States

The Supreme Court of the United States upheld the Affordable Care Act as constitutional in the landmark decision for National Federation of Independent Business v. Sebelius.

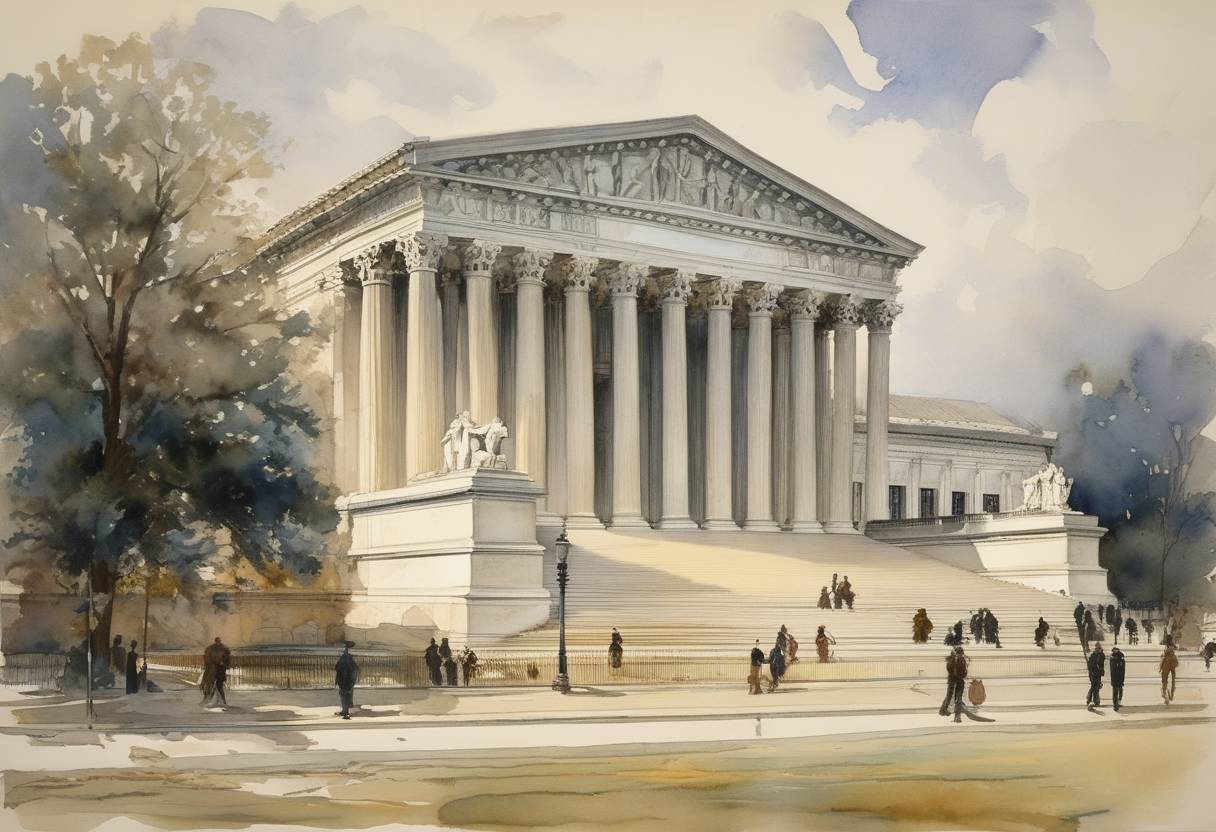

April 8, 1895

The Supreme Court of the United States ruled in Pollock v. Farmers' Loan & Trust Co., determining that unapportioned income taxes on interest, dividends, and rents were unconstitutional.

Washington D.C., United States | Supreme Court of the United States

On April 8, 1895, the Supreme Court of the United States delivered a landmark decision in the case of Pollock v. Farmers’ Loan & Trust Co., addressing the constitutionality of federal income taxes that were unapportioned among the states. This pivotal decision had a significant impact on the fiscal policies of the United States, steering the course of taxation legislation until the adoption of the 16th Amendment in 1913.

The case was brought to the Supreme Court by Charles Pollock, a shareholder in Farmers’ Loan & Trust Company, who contested the company’s intention to comply with the 1894 federal income tax law. This law imposed taxes on incomes exceeding $4,000, including personal income derived from interest, dividends, and rents.

Pollock argued that this tax was effectively a direct tax on property without apportionment among the states based on population, as mandated by the Constitution. According to the prevailing interpretation of the Constitution at the time, direct taxes were required to be apportioned among the states according to their populations, a condition the income tax law did not meet.

The Supreme Court, in a divided opinion, ruled in favor of Pollock. The Court held that the portions of the 1894 income tax law imposing taxes on income derived from property—such as interest, dividends, and rents—constituted a direct tax. Consequently, since these taxes were not apportioned according to the states’ populations, the Court found them unconstitutional.

Chief Justice Melville Fuller led the majority opinion, emphasizing that taxes on the income from property were direct taxes, hence requiring apportionment under the Constitution. This interpretation rendered substantial parts of the 1894 income tax statute invalid, effectively nullifying the law.

The decision in Pollock v. Farmers’ Loan & Trust Co. underscored the limitations of federal power to levy direct taxes, catalyzing a re-evaluation of the U.S. tax system. The ruling severely restricted the federal government’s capacity to levy income taxes, which were viewed as a progressive tool for generating revenue and addressing fiscal inequalities.

The ramifications of the decision were profound, contributing to the eventual passage of the 16th Amendment in 1913. This amendment provided the constitutional basis for Congress to levy an income tax without apportionment among the states, fundamentally transforming the landscape of American taxation and enabling the modern federal income tax system.

In the broader context, the ruling marked a critical moment in the evolution of constitutional law regarding federal-state power dynamics and fiscal policy, reflecting the tensions and disagreements over the scope of Congressional taxation authority that had persisted since the founding of the Republic.

Source: www.oyez.org